August 29, 2018

Flood insurance guide

By Insurance.com Posted : August 28, 2017 lightly amended by RAMP.

Flooding is the most common natural disaster in the United States. It's also the most expensive, costing homeowners, insurers and the government billions each year. If most of your wealth is tied up in your house, you may be risking financial ruin without adequate flood insurance coverage.

This guide tells you what flood insurance covers, how much it costs, how it works, and who should consider having it.

Does homeowners insurance cover flooding?

Homeowners insurance typically covers water damage from bursting pipes and overflowing toilets, sinks and tubs. It usually covers the costs if your dishwasher or water heater explodes. If you buy a special endorsement, your homeowners policy also reimburses expenses incurred from sewer or water line backups.

Your homeowners insurance also kicks in if a storm like a hurricane blows your roof off and your interiors are damaged by rain. You’re covered by homeowners insurance as long as the water originates from within your home or directly from the sky.

However, your homeowners insurance (and umbrella policy, if you have one) typically does not cover damage caused by water that has come in contact with the ground outside -- from rising water from creeks, rivers, flash flooding, etc. You can only get that protection from a flood insurance policy.

That being said, an extra rider on a homeowners insurance policy might help to elevate a structure. If a fire or wind damage caused the house to be substantially damaged, and to rebuild you would have to elevate, this coverage could come in handy. Ordinance and Law Coverage may be available on the homeowner policy to pay for coming into compliance with the flood ordinance if the insurance policy is paying for a covered loss as well. It wouldn’t be available after a flood if that was the only insurance claim from an event, but it might help elevate the structure after a fire or wind event. See the FloodSafe Minute from April 2017 or call your agent for more information.

Who needs flood insurance?

Once you know how limited your homeowners coverage is, you may be asking yourself, "Do I need flood insurance?"

Mortgage lenders require home buyers in designated flood plains (aka Special Flood Hazard Areas, or SFHAs) to purchase flood insurance. If you don't live in a flood plain or have a mortgage, you won't be forced to buy flood coverage.

Even if you're not required to buy flood insurance, however, you should consider it. According to the Insurance Information Institute, more than one-fifth of claims for flood damage originate in homes that are in low-to-moderate risk areas -- households that are not required to purchase flood insurance by lenders.

As the experts at the National Flood Insurance Program say, "Everyone lives in a flood zone."

Most of the people who flooded in Houston and central Louisiana could have gotten flood insurance for under $500/year, but didn’t because it wasn’t required. They are not at the mercy of the federal tax payer to build back. In fact, one-third of all flood-related disaster assistance, which is available to uninsured homeowners, went to those not in designated flood plains. The fact that one in five flood claims originate outside high-risk areas, while scary, doesn’t capture the cost to uninsured homeowners. That's because only about 12 percent of homeowners nationwide have flood insurance, so many of those affected by floods had no policies to collect on and therefore the flood devastation is often underestimated.

Without insurance, disaster relief from floods mostly takes the form of low-interest loans made available by the federal government (ask about SBA and 203 (k) loans). These loans must be paid back. Purchasing a flood insurance policy is the only way to fully protect your family from flood-related costs.

How does flood insurance work?

National flood insurance is administered by the federal government and sold only through licensed insurance agents. Unlike most other types of insurance, flood insurance policy rates should not vary between insurers. However, a more skilled insurance agent may know how to document safety features of your home or business to get discounts, or know how to select a price that is better for you. Sometimes buying more coverage is a lower premium!

You can insure your house for up to $250,000 and your personal property (contents) for up to $100,000. If you rent, you can buy up to $100,000 in coverage for your belongings. For non-residential property, you can buy up to $500,000 of coverage for the building and contents.

Flood insurance does come with separate deductibles for the building and its contents. You get to choose the deductible amount. Higher deductibles get you lower premiums; however, if you have a mortgage, your lender may not allow you to increase your deductible beyond specified limits.

Understand that flood insurance does not kick in immediately, so you can't just buy it once a storm is heading your way. There's a 30-day waiting period in most cases.

However, there are a few exceptions:

- If your address was newly-added to the SFHA map and you buy flood insurance within the 13-month period following a map revision.

- If you're renewing your flood policy and increase your coverage.

- If your home is affected by flooding on burned federal land and you buy a policy within 60 days of the fire's containment.

- If you just bought a house and your lender requires flood coverage.

If you wait until the rainy season to buy your flood policy, you could be trapped in a nightmare scenario -- having purchased insurance but ineligible for coverage if a storm hits within a month. For maximum peace of mind, it may be best to "set it and forget it."

Flood insurance FAQs

Here are some common flood insurance questions:

Can I get flood insurance even if my lender doesn't require it?

Yes, and if you're in a lower-risk area, you may qualify for Preferred Risk Policy (PRP) rates.

Can I get flood insurance if I have filed flood insurance claims before?

Yes, you can get flood insurance if the property has been flooded previously. Your premium may reflect the added risk of subsequent flooding as the PRP is not available for properties with two or more floods. However, in general, the costs of the premium is based on location in the floodplain and perceived risk rather than the number of claims.

Can I pay a monthly premium for flood insurance?

No, you have to pay for a full year, upfront. The NFIP accepts checks, Master Card, Visa, and AmEx. Legislation from 2014 appears to allow for monthly or quarterly payments to make flood insurance more accessible to lower income families, but that does not appear to have been adopted by any write your own company or the federal government at NFIP direct.

My home and contents are worth more than $350,000. Can I buy additional coverage?

While the NFIP does not offer extended coverage, many private insurers do. Their rates are not regulated, so you'll need to shop with competing providers to get the best rates. Reinsurance is an option, and one can buy the policy entirely from a private insurer. Be aware that certain grant programs will not be available to any structure that is insured through a private insurance policy, and private insurance is not required to provide the same benefits as an NFIP policy.

How do I find out what my flood risk is?

For the flood risk assigned by the Federal Emergency Management Agency (FEMA) flood zones are mapped nationwide. You can enter your address into the flood risk tool provided by FEMA to see your local risk profile. In Louisiana you can get a basic idea from http://maps.lsuagcenter.com/floodmaps. Call your Floodplain Administrator for a legal interpretation of your flood zone. Ask the neighbors to see if it has flooded regardless of zone.

My house is on a hill and will never be flooded, though it's in a flood zone. Can I get out of buying flood insurance?

First, even houses on a hill can flood whether that be a basement, a mudslide or a flashflood from higher areas. However, local areas within flood zones may not be considered high risk if the home is higher than the designated Base Flood Elevation, or BFE. To get an exemption, you can submit property and elevation materials with a Letter of Map Amendment (LOMA). For detailed information, call FEMA toll-free at 1.877.336.2627. Your local floodplain manager will have to sign off on the request as part of the submission, but it is your responsibility to make the case that your structure is not at high risk.

What does flood insurance cover?

Flood insurance losses directly resulting from flooding or flood-related erosion caused by heavy or prolonged rain, snow melt, coastal storm surges, blocked storm drainage systems, levee dam failure and similar events.

Flood insurers reimburse policyholders for structural damage, including:

- The insured building and its foundation.

- The electrical and plumbing systems.

- Central air-conditioning systems, furnaces, and water heaters.

- Refrigerators, cooking stoves, and built-in appliances like dishwashers and trash compactors.

- Permanently installed carpeting and flooring.

- Permanently installed paneling, wallboard, and built-in bookcases and cabinets.

- Window blinds and shutters.

- Detached garages (up to 10 percent of structural coverage). Other outbuildings require separate policies.

- Debris removal.

In addition, flood insurance covers damage and loss of personal property as follows:

- Clothing, furniture, and electronics.

- Curtains and window treatments.

- Portable and window air-conditioners.

- Portable microwave ovens, dishwashers and other small appliances.

- Rugs.

- Clothes washers and dryers.

- Food freezers and the food in them.

- Valuables like artwork, jewelry and furs (up to $2,500).

If you have a lot of valuables, ask your insurer about additional riders or endorsements to extend your flood coverage.

What does flood insurance not cover?

Flooding in the first 30 days

Standard flood insurance plugs many holes in your homeowners policy, but it's not fool-proof. As indicated above, your coverage will not kick in if purchased less than 30 days prior to the occurrence of flood damage.

"We always encourage people to educate themselves on what their home's risk might be, and talk to their insurance agent well before there's a storm on the horizon or any type of flooding situation that would come up," says Christina Loznicka, a spokesperson for Allstate Insurance in Northbrook, Ill.

Damages exceeding policy limits

In addition, federal flood insurance coverage is capped at $350,000 -- $250,000 for your dwelling and $100,000 for your personal possessions, says Rachel Racusen, a spokeswoman for FEMA. If your house or the property in it is valued at more than those limits, you could be at risk of being underinsured.

To protect yourself and your belongings, it's important to determine if you need additional coverage, says Loznicka. "Ask your insurance agent if you're eligible to purchase excess flood insurance, which is offered by private insurers."

Such policies can provide up to several million dollars of extra coverage. Policyholders must first purchase NFIP coverage before they can buy the extra coverage, which has widely varying

Landscaping and exterior features

If a flood takes out your trees or plants, you're out of luck. Also excluded are features like fountains, decks, patios, walkways, fences, hot tubs, swimming pools, wells and septic systems.

Living expenses

If your home becomes unlivable in the wake of a flood, your insurance will not cover the cost of alternative living arrangements. While your standard homeowners policy does include this for other disasters, it does not apply to flooding. You may be able to purchase additional coverage -- ask your agent.

Miscellaneous

Other items excluded from flood coverage include:

- Damage caused by moisture, mildew, or mold that could have been prevented by you

- Currency, precious metals, and valuable papers like stock certificates

- Financial losses caused by the loss of use of the property

- Vehicles

Cost of flood insurance

How much is flood insurance? That depends. If your home is located in a low-to-moderate risk area, you're eligible for Preferred Risk Policy (PRP) rates. These are standard for the amount of coverage you desire and come with a minimum $1,000 deductible. The table below shows PRP rates for varying amounts of coverage.

How much is flood insurance for those in flood zones?

For those in higher-risk areas (Zones V and A), the cost of coverage depends on your home's size, construction, location, and your deductible. According to FEMA, the average flood insurance policy costs about $700 per year, but can vary wildly, depending on your home's elevation.

The Base Flood Elevation, or BFE shown on the Flood Insurance Rate Map (FIRM) for high-risk flood zones indicates the water surface elevation resulting from a flood that has a 1 percent chance of equaling or exceeding that level in any given year.

The primary way to reduce your flood insurance cost is to increase your home's elevation. Going from four feet below the BSE to three feet above it would save over $90,000 in 10 years at today's premiums. Homeowners may be able to get low-cost loans or grants to accomplish this.

The other way to lower costs is to increase your deductible. The minimum deductible for flood insurance is $1,000, and the maximum deductible is $10,000. You can save up to 40 percent on your premiums by increasing your deductible.

For those in the riskiest areas, the savings realized by increasing to a $10,000 deductible would make up the added cost in less than three years. However, if a homeowner doesn’t have the $10,000, some companies will not pay until the $10,000 is invested first. Therefore, it could put the claim at risk.

Cost of not having flood insurance

FloodSmart.gov has created a damage estimator tool to show the potential effects of a flood in your home. You can access it here.

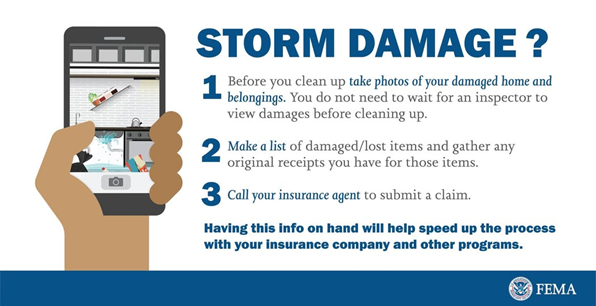

How do you file a flood insurance claim?

The process consists of five steps.

1. Contact your insurer as soon as possible. All flood insurance policies require you to give timely written notice of loss. Have your policy number and a phone number and/or e-mail address where you can be reached.

2. Separate your damaged and undamaged property. Don't dispose of anything before an adjuster has seen it, unless required by law. If you have to get rid of anything (for instance, mold-infested carpet), take pictures and keep samples of the damaged goods (a small piece of the carpet).

You need to do whatever you can to prevent further damage and protect undamaged property, but you'll want to consult with your flood adjuster or flood insurer before hiring anyone to do repairs.

3. Compile a list of damaged personal property. It's smart to create a list before flooding, so all you have to do is check off the items that are damaged. The list should have an item description, cost, model and serial number (when applicable), and estimated dollar loss. Include any receipts, photos, and warranties you have.

4. Detail structural damages. Note structural loss/damage to point out to the insurance adjuster. Your adjuster will usually contact you within 24-48 hours after being notified of your loss. Then, he or she will come view your property. You may ask the adjuster for an advance or partial payment. If you have a mortgage, your mortgage company will need to sign the Building Property advance check.

5. Complete a Proof of Loss statement containing the information required by your flood insurance policy within 60 days after the loss. The Proof of Loss includes a detailed estimate to replace or repair the damaged structure and contents. In most cases, the adjuster can provide you with a suggested Proof of Loss.

Your claim is payable after you and the insurer agree on the amount of damages, and the insurer receives your complete, accurate and signed Proof of Loss in support of your claim.

How to get flood insurance

You can simply call the company that provides your homeowners insurance to add flood coverage.

"Flood costs are based on your risk in an area, and is priced the same from the federal government's National Flood Insurance Program," says Loretta Worters, vice president of communications at the Insurance Information Institute. "Prices tend to be higher when flood insurance is unavailable through the NFIP."

There may be differences in the service offered by various providers, however. Worters explains, "All insurers should handle the claims the same: the claims that have the most damage are likely to be handled first. Service is of course a factor. The best way to find out the service provided by an insurer is to ask friends, family and neighbors what their experiences have been like."

If your current carrier does not offer flood insurance, you can find homeowners and flood insurance referrals by contacting the NFIP at 888-379-9531 for an agent referral.

Related Information 1

Guide in PDF - Charts and Visuals